Fill Out Your Aar Prequal Form

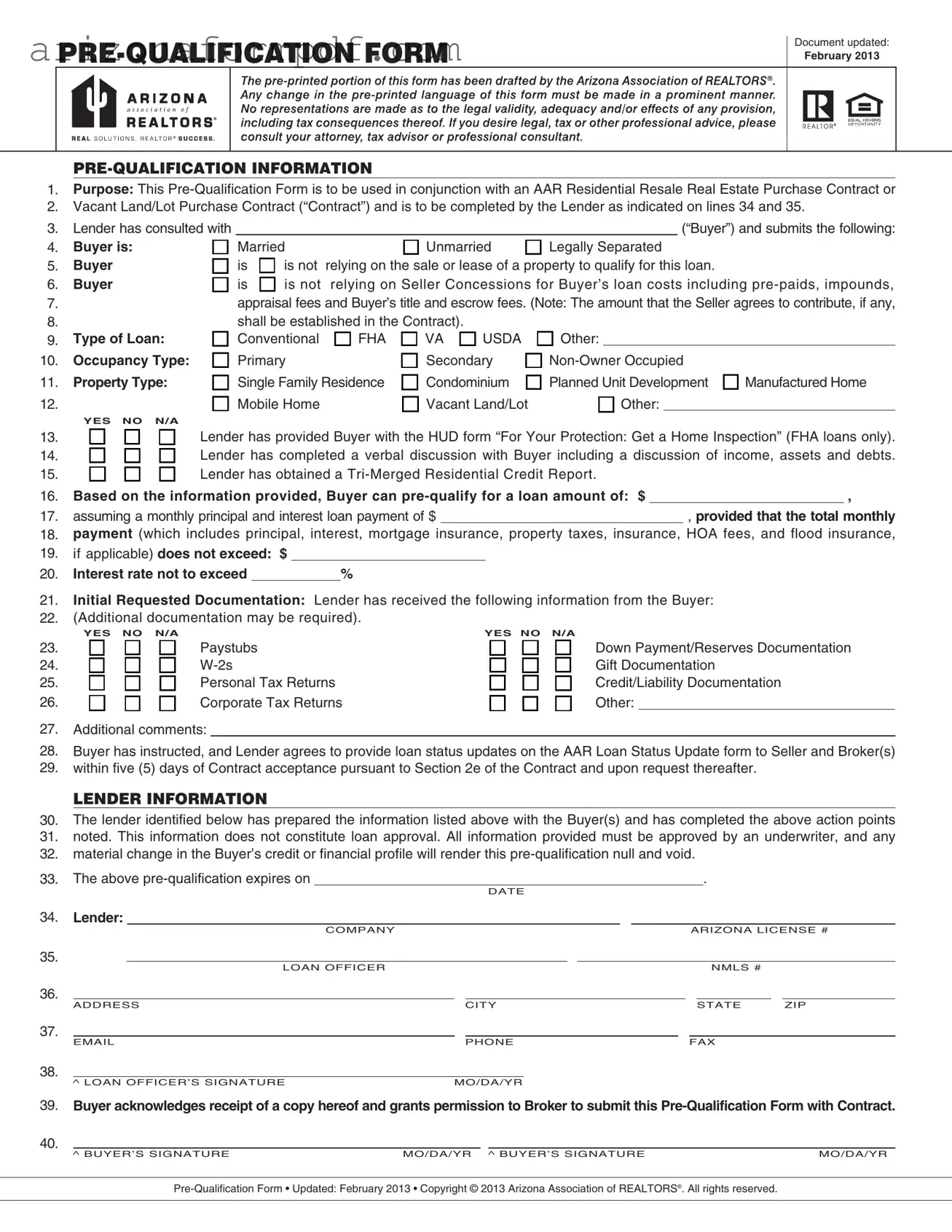

The AAR Prequal Form serves as a vital tool in the home buying process, providing essential information for both buyers and lenders. Designed to accompany an AAR Residential Resale Real Estate Purchase Contract or a Vacant Land/Lot Purchase Contract, this form lays the groundwork for a successful transaction. It begins with a series of questions aimed at understanding the buyer's marital status, financial reliance on property sales, and whether they will depend on seller concessions for loan costs. The form further delineates the type of loan being sought—whether it be conventional, FHA, VA, USDA, or other—and specifies the intended occupancy type, be it primary, secondary, or non-owner occupied. Additionally, it identifies the property type, including options like single-family residences and condominiums. Lenders are required to engage in a thorough discussion with buyers, covering their income, assets, and debts, and to provide a Tri-Merged Residential Credit Report. Notably, the prequalification does not imply loan approval; rather, it serves as an initial assessment of the buyer’s potential eligibility for a loan amount, contingent upon various financial factors. It is important to note that the prequalification is valid for a limited time and can be rendered void by any significant changes in the buyer's financial situation. This form ultimately facilitates clear communication between all parties involved, ensuring that buyers are well-informed as they navigate the complexities of purchasing a property.

Guide to Writing Aar Prequal

After completing the AAR Prequal form, the next steps involve submitting the form to the appropriate parties, typically the lender and real estate agents involved in the transaction. This document will help facilitate the loan process and ensure all necessary parties are informed about the buyer's financial readiness.

- Begin by entering the purpose of the form, which is to be used with a residential resale real estate purchase contract or a vacant land/lot purchase contract.

- Fill in the buyer’s marital status by selecting one of the following options: Married, Unmarried, or Legally Separated.

- Indicate whether the buyer is relying on the sale or lease of a property to qualify for the loan by checking the appropriate box.

- Specify if the buyer is relying on seller concessions for loan costs, including pre-paids, appraisal fees, and title and escrow fees.

- Select the type of loan the buyer is applying for: Conventional, FHA, VA, USDA, or Other.

- Choose the occupancy type: Primary, Secondary, or Non-Owner Occupied.

- Identify the property type: Single Family Residence, Condominium, Planned Unit Development, or Manufactured Home.

- Indicate if the property is a mobile home, vacant land/lot, or other by checking the relevant boxes.

- Confirm whether the lender has provided the buyer with the HUD form “For Your Protection: Get a Home Inspection” if applicable.

- Check if a verbal discussion regarding income, assets, and debts has been completed with the buyer.

- Verify if a Tri-Merged Residential Credit Report has been obtained.

- Fill in the pre-qualification loan amount the buyer can qualify for, along with the monthly payment details.

- State the interest rate not to exceed.

- List the initial requested documentation received from the buyer, marking the appropriate boxes for paystubs, W-2s, tax returns, and other relevant documents.

- Provide any additional comments if necessary.

- Fill in the lender information, including company name, license number, loan officer details, and contact information.

- Sign and date the form in the designated areas for both the lender and the buyer.

Browse Popular Forms

Does Arizona Have Sales Tax - Any misuse may have serious consequences for the purchaser.

Arizona Financial - Filing this affidavit is often mandatory for both sides in divorce or custody cases.

State Taxes Arizona - The Arizona Department of Revenue will determine eligibility based on the submitted information.

Common Questions

What is the purpose of the AAR Prequal Form?

The AAR Prequal Form is designed to help buyers obtain pre-qualification for a loan. It is used alongside the AAR Residential Resale Real Estate Purchase Contract or the Vacant Land/Lot Purchase Contract. The lender completes this form after consulting with the buyer to assess their financial readiness for a loan.

Who completes the AAR Prequal Form?

The lender is responsible for completing the AAR Prequal Form. They will gather information from the buyer regarding their financial situation and submit the necessary details as indicated in the form.

What information does the buyer need to provide?

The buyer must provide various details, including their marital status, whether they are relying on the sale of another property or seller concessions, and the type of loan they are seeking. Additionally, they need to submit documentation such as pay stubs, tax returns, and down payment information.

What types of loans can be indicated on the form?

Buyers can indicate several types of loans on the AAR Prequal Form. These include Conventional, FHA, VA, USDA, and other loan types. This helps the lender understand the buyer's preferred financing options.

What does pre-qualification mean?

Pre-qualification means that the lender has reviewed the buyer's financial information and believes they may qualify for a loan. However, it is important to note that this does not guarantee loan approval. An underwriter must still review and approve all information provided.

How long is the pre-qualification valid?

The pre-qualification is valid until the expiration date indicated on the form. If there are any significant changes in the buyer's financial situation, the pre-qualification may become null and void.

Will the lender provide updates on the loan status?

Yes, the lender agrees to provide loan status updates to the seller and brokers within five days of contract acceptance. This is done using the AAR Loan Status Update form and will continue upon request thereafter.

Dos and Don'ts

When filling out the AAR Prequal form, it is important to follow certain guidelines to ensure that the process goes smoothly. Here is a list of things to do and avoid:

- Do provide accurate personal information, including marital status and property details.

- Do indicate whether you are relying on the sale of another property or seller concessions.

- Do specify the type of loan you are applying for, such as Conventional, FHA, or VA.

- Do ensure that all required documentation, like paystubs and tax returns, is ready for submission.

- Don't leave any sections blank; incomplete forms can lead to delays.

- Don't provide false information, as this can invalidate your pre-qualification.

- Don't forget to sign and date the form; your acknowledgment is crucial.

- Don't assume verbal discussions with the lender are sufficient; always confirm in writing.

Similar forms

The Loan Estimate (LE) form is similar to the AAR Prequal form in that it provides crucial information about the loan terms and costs. The LE is required by law and must be provided to borrowers within three business days of applying for a loan. Like the Prequal form, it outlines the loan amount, interest rate, and estimated monthly payments. Both documents also include details about the costs associated with obtaining the loan, such as closing costs and fees, making it easier for borrowers to understand their financial obligations.

The Good Faith Estimate (GFE) serves a similar purpose to the AAR Prequal form by offering an overview of the costs and terms of a mortgage. Although the GFE has been largely replaced by the LE, it still shares many characteristics with the Prequal form. Both documents aim to give borrowers a clear picture of what to expect financially. The GFE includes estimated closing costs, interest rates, and monthly payments, allowing buyers to compare different loan options effectively.

The Uniform Residential Loan Application (URLA) is another document that aligns closely with the AAR Prequal form. The URLA collects detailed information about the borrower’s financial situation, including income, assets, and debts. Like the Prequal form, it is used by lenders to assess a borrower's eligibility for a loan. Both documents require similar personal information and help lenders evaluate the risk associated with lending to a particular borrower.

The Pre-Approval Letter is similar to the AAR Prequal form in that it indicates a borrower’s eligibility for a loan based on preliminary information. While the Prequal form gives a rough estimate of what a buyer can afford, the Pre-Approval Letter is a more formal acknowledgment from the lender that the borrower meets certain criteria. Both documents are essential in the home-buying process, as they signal to sellers that the buyer is serious and has the financial backing to proceed with a purchase.

The Financial Disclosure Statement (FDS) is another document that shares similarities with the AAR Prequal form. The FDS provides a comprehensive overview of the borrower’s financial health, including income, debts, and assets. Like the Prequal form, it assists lenders in determining the borrower’s ability to repay the loan. Both documents aim to ensure that borrowers fully understand their financial situation before committing to a mortgage.

The Debt-to-Income Ratio (DTI) analysis is an essential component that relates closely to the AAR Prequal form. DTI is a measure used by lenders to assess a borrower's financial stability by comparing their monthly debt payments to their gross monthly income. The Prequal form includes questions about income and debts, which are necessary to calculate the DTI. Both tools help lenders evaluate whether a borrower can afford the loan they are seeking.

The Closing Disclosure (CD) is similar to the AAR Prequal form in that it details the final terms and costs of the mortgage. While the Prequal form provides an initial estimate, the CD presents the actual costs that the borrower will face at closing. Both documents are designed to inform borrowers about their financial commitments, ensuring they understand the implications of their loan before finalizing the purchase.

Finally, the Borrower’s Authorization form is akin to the AAR Prequal form as it grants permission for the lender to obtain the borrower’s credit report and other financial information. This form is essential for the lender to assess the borrower’s creditworthiness, similar to the information collected in the Prequal form. Both documents are crucial for the loan approval process and help streamline communication between the borrower and lender.

Key takeaways

When filling out the AAR Prequal form, it’s important to keep several key points in mind to ensure a smooth process. Here are some essential takeaways:

- Understand the Purpose: This form is meant to be used alongside a Residential Resale Real Estate Purchase Contract or a Vacant Land/Lot Purchase Contract. It helps establish whether a buyer can pre-qualify for a loan.

- Provide Accurate Information: The lender must gather detailed information about the buyer’s marital status, financial situation, and property type. This includes whether the buyer relies on seller concessions or the sale of another property to qualify for the loan.

- Documentation is Key: The lender should collect necessary documentation such as paystubs, tax returns, and down payment information. This documentation is crucial for the lender to assess the buyer’s financial health.

- Stay Informed: The lender is responsible for keeping the buyer updated on the loan status. Updates should be provided within five days of contract acceptance, ensuring that all parties are on the same page.

By following these guidelines, buyers and lenders can effectively navigate the pre-qualification process, leading to a more efficient home-buying experience.

Common mistakes

-

Incomplete Personal Information: Many individuals forget to fill in all the required personal details, such as marital status and occupancy type. Missing this information can lead to delays in processing the application.

-

Misunderstanding Loan Type: Selecting the wrong loan type can create confusion. It’s essential to choose the correct option, whether it’s Conventional, FHA, VA, or USDA, to ensure the right guidelines are followed.

-

Ignoring Seller Concessions: Buyers often overlook the section regarding reliance on seller concessions. Clearly indicating whether seller contributions will be used for loan costs is crucial for accurate pre-qualification.

-

Omitting Required Documentation: Failing to provide necessary documentation, such as paystubs or tax returns, can hinder the pre-qualification process. Ensure all requested documents are submitted to avoid delays.

-

Inaccurate Financial Information: Providing incorrect income or debt figures can lead to miscalculations in loan eligibility. Double-check all financial details for accuracy before submission.

-

Not Acknowledging Expiration Date: Some buyers forget to note the expiration date of the pre-qualification. This can lead to confusion later, as the pre-qualification is only valid for a limited time.

Document Preview

Document updated:

February 2013

1.Purpose: This

2.Vacant Land/Lot Purchase Contract (“Contract”) and is to be completed by the Lender as indicated on lines 34 and 35.

3. |

Lender has consulted with |

|

|

|

|

|

|

|

|

|

|

(“Buyer”) and submits the following: |

||||||

4. |

Buyer is: |

|

N Married |

|

N Unmarried |

N Legally Separated |

|

|

||||||||||

5. |

Buyer |

|

|

N is |

N is not |

relying on the sale or lease of a property to qualify for this loan. |

|

|

||||||||||

6. |

Buyer |

|

|

N is |

N is not |

relying on Seller Concessions for Buyer’s loan costs including |

||||||||||||

7. |

|

|

|

|

appraisal fees and Buyer’s title and escrow fees. (Note: The amount that the Seller agrees to contribute, if any, |

|||||||||||||

8. |

|

|

|

|

shall be established in the Contract). |

|

|

|

|

|

|

|

|

|

||||

9. |

Type of Loan: |

N Conventional |

N FHA |

N VA N USDA |

|

N Other: |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

||||||||||||

10. |

Occupancy Type: |

N Primary |

|

N Secondary |

N |

|

|

|||||||||||

11. |

Property Type: |

N Single Family Residence |

N Condominium |

N Planned Unit Development |

N Manufactured Home |

|||||||||||||

12. |

YES |

NO |

N/A |

N Mobile Home |

|

N Vacant Land/Lot |

N Other: |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

13. |

N |

N |

N |

Lender has provided Buyer with the HUD form “For Your Protection: Get a Home Inspection” (FHA loans only). |

||||||||||||||

14. |

N |

N |

N |

Lender has completed a verbal discussion with Buyer including a discussion of income, assets and debts. |

||||||||||||||

15. |

N |

N |

N |

Lender has obtained a |

|

|

||||||||||||

16. |

Based on the information provided, Buyer can |

|

|

, |

||||||||||||||

17. |

assuming a monthly principal and interest loan payment of $ |

|

|

|

|

|

|

|

, provided that the total monthly |

|||||||||

18.payment (which includes principal, interest, mortgage insurance, property taxes, insurance, HOA fees, and flood insurance,

19.if applicable) does not exceed: $

20. Interest rate not to exceed |

|

% |

21.Initial Requested Documentation: Lender has received the following information from the Buyer:

22.(Additional documentation may be required).

YES NO N/A |

YES NO N/A |

23.

24.

25.

26.

N

N

N

N

N |

N |

N |

N |

N |

N |

N |

N |

Paystubs

Personal Tax Returns

Corporate Tax Returns

N

N N

N N

N N

N N

N N

N N

N

N

N

N

N

N

Down Payment/Reserves Documentation

Gift Documentation

Credit/Liability Documentation

Other:

27.Additional comments:

28.Buyer has instructed, and Lender agrees to provide loan status updates on the AAR Loan Status Update form to Seller and Broker(s)

29.within five (5) days of Contract acceptance pursuant to Section 2e of the Contract and upon request thereafter.

LENDER INFORMATION

30.The lender identified below has prepared the information listed above with the Buyer(s) and has completed the above action points

31.noted. This information does not constitute loan approval. All information provided must be approved by an underwriter, and any

32.material change in the Buyer’s credit or financial profile will render this

33. |

The above |

|

|

|

|

. |

|

|

|||||||||

|

|

|

|

|

|

DATE |

|

|

|

|

|

|

|

|

|

||

34. |

|

Lender: |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

COMPANY |

|

|

|

|

|

|

|

|

ARIZONA LICENSE # |

||||

35. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LOAN OFFICER |

|

|

|

|

|

|

|

|

|

|

NMLS # |

|

|

|

36. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ADDRESS |

CITY |

|

|

|

|

|

STATE |

|

ZIP |

||||||

37. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PHONE |

|

|

|

|

FAX |

|

|

|||||||

38.

^ LOAN OFFICER’S SIGNATURE |

MO/DA/YR |

39.Buyer acknowledges receipt of a copy hereof and grants permission to Broker to submit this

40.

^ BUYER’S SIGNATURE |

MO/DA/YR ^ BUYER’S SIGNATURE |

MO/DA/YR |

Form Breakdown

| Fact Name | Description |

|---|---|

| Purpose | The AAR Pre-Qualification Form is intended for use with the AAR Residential Resale Real Estate Purchase Contract or Vacant Land/Lot Purchase Contract. It is to be completed by the lender after consulting with the buyer. |

| Loan Types | Buyers can choose from various loan types, including Conventional, FHA, VA, USDA, and others. Each type may have specific requirements and conditions. |

| Occupancy Types | The form allows buyers to indicate the occupancy type of the property, which can be Primary, Secondary, or Non-Owner Occupied. This classification can affect loan terms. |

| Documentation Requirements | Lenders must receive initial documentation from buyers, which may include paystubs, W-2s, personal tax returns, and credit documentation. Additional documentation may be required later. |

| Expiration of Pre-Qualification | The pre-qualification provided by the lender is valid until a specified expiration date. Any significant change in the buyer's financial profile can nullify the pre-qualification. |